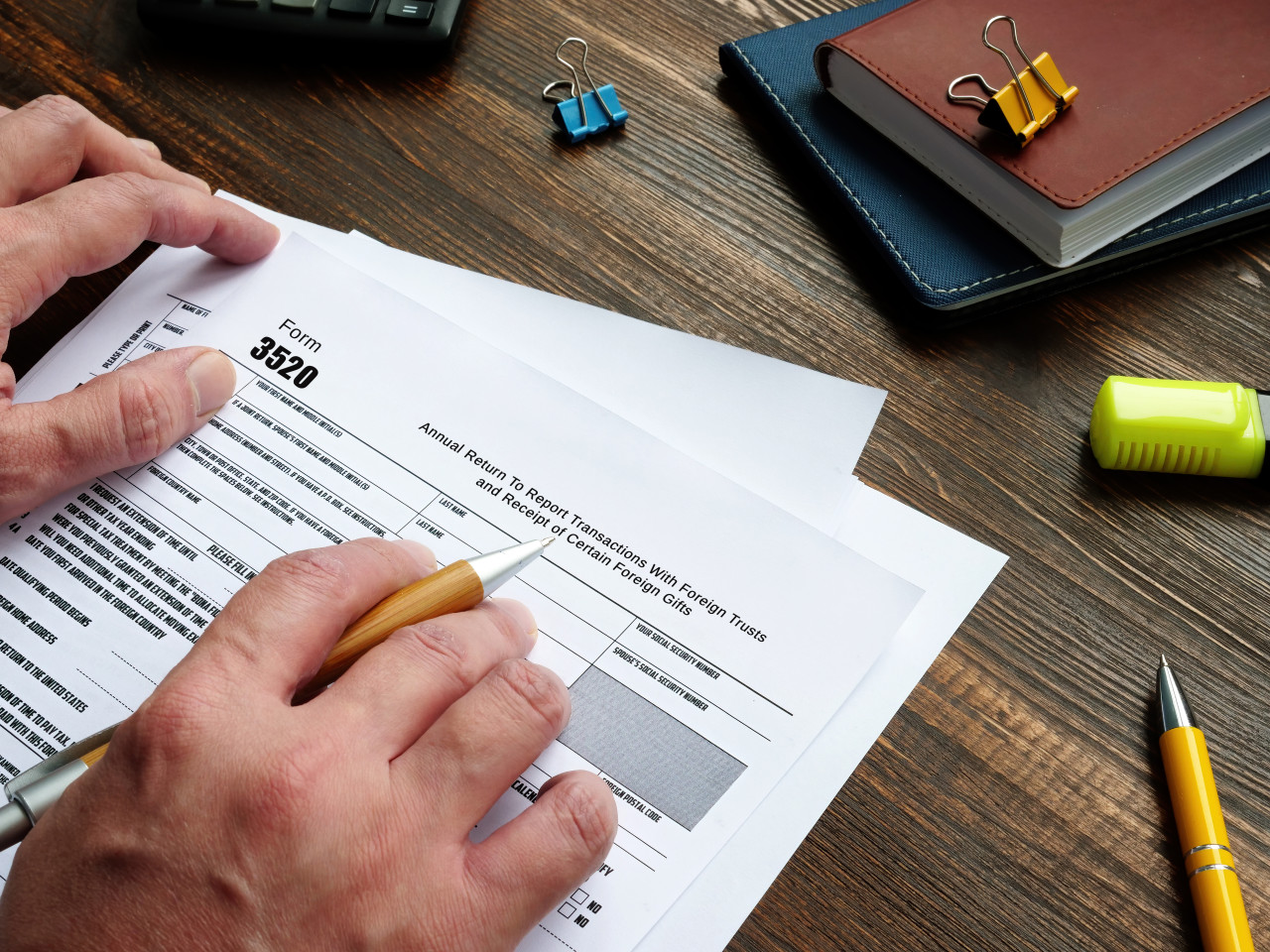

Over the past decade, the IRS has intensified scrutiny on foreign asset reporting, with non-compliance leading to severe tax penalty implications, including hefty fines and criminal charges for U.S. taxpayers. Though we have already discussed at length the FBAR and Form 8938, this article will take a deeper dive into one of the most common international information reporting forms - Form 3520. Who is Required to Report? U.S. taxpayers are obliged under tax law to report global income. "United States Persons" who must report include:U.S. citizens or residentsDomestic partnerships and corporationsU.S. estates (excluding foreign ones)Trusts under U.S. jurisdictionOthers not classified as...

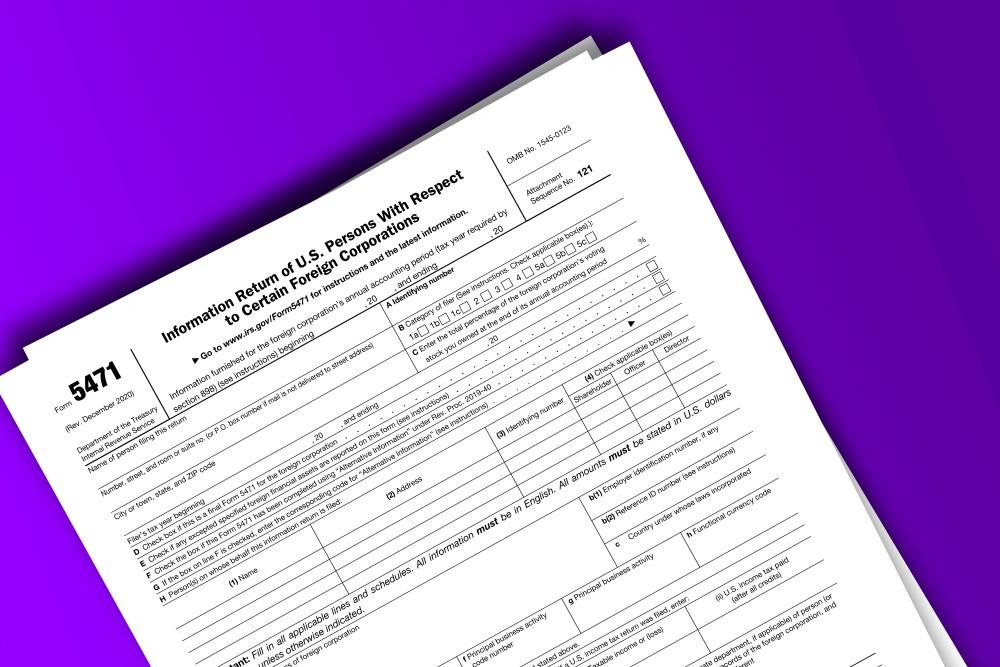

An Introduction to Form 5471 - Information Return of U.S. Persons With Respect to Certain Foreign Corporations Purpose of Form Form 5471 is used to satisfy the reporting requirements of Internal Revenue Code (“IRC”) §§ 6038 (information reporting with respect to certain foreign corporations and partnerships) and 6046 (returns as to organization or reorganization of foreign corporations and as to acquisitions of their stock). Likewise, Form 5471 is used to report amounts related to IRC § 965 (treatment of deferred foreign income upon transition to participation exemption system of taxation). Certain U.S. persons who are officers, directors, or shareholders in...

Under the Bank Secrecy Act, formerly known as the Currency and Foreign Transactions Report Act of 1970, Congress enacted the requirement that certain foreign bank and financial accounts must be reported by United States taxpayers by filing a Report of Foreign Bank and Financial Accounts (“FBAR”). What is an FBAR? An FBAR is a Foreign Bank Account and Financial Asset Report, which is filed on FinCEN Form 114. Congress’s rationale for requiring the reporting of foreign bank accounts and financial assets is simple – to prevent tax evasion. Although the IRS retains civil FBAR enforcement authority, FinCEN Form 114...

A recent appeals court ruling seems to leave the possibility open, and provides taxpayers a different reason to be particularly worried. Millions of people play online poker. One of the most popular games in the country is, of course, Texas Hold 'Em, and it's a virtual requirement to know the basics if you're a resident of the Lone Star State. A recent ruling by the Ninth Circuit Court of Appeals in San Francisco - while not controlling in Texas - seems to lean toward the idea that at least some online gambling accounts will be considered "financial accounts" for purposes of...

With the tax filing deadline just a couple of weeks away, most U.S. taxpayers have April 15th circled on their calendars as the date by which they'll have to let the IRS in on how much they expect back, or more likely (if you're reading this) how much the IRS should expect from them. For most, April 15th marks the end of "tax season" and they can breath easy for another year until the next go-round. But for U.S. taxpayers that have foreign accounts which they've not previously disclosed on Schedule B of their tax return nor filed the required "FBAR"...

In March, the IRS announced that it will be closing the Offshore Voluntary Disclosure Program ("OVDP"), shutting the door on the best opportunity for taxpayers with previously undisclosed foreign accounts and assets to come forward without facing civil penalties that can amount to 3-4 times the value of their total foreign accounts and/or assets. The first iteration of the IRS' OVDP program was made available in 2009, and since then, the IRS has made considerable progress (through the signing of many intergovernmental agreements with other countries and the increased information sharing resulting from them) in identifying taxpayers with unreported offshore accounts and/or assets. On top...

With April 15th now less than one week away, taxpayers and their CPAs are busy gathering any additional information necessary to complete their returns on time. In some cases, that information can't be realistically obtained in time to make sure the return will be filed correctly, so thousands of taxpayers will (or already have) submit Form 4868, which grants an automatic extension of the deadline to file the tax return for 6 months. For taxpayers with foreign bank accounts that have yet to be disclosed to the IRS via the normal FBAR filing requirement or, alternatively, through one of the IRS'...